Unlocking the Power of Fixed Income

Episode 6

Types of Bonds: Government, Corporate, and More

Introduction

Bonds come in many forms, each serving a different role in an investment portfolio. From low-risk government bonds to higher-yielding corporate debt, understanding the various bond types helps investors tailor their portfolios to their financial goals and risk tolerance.

In this episode, we’ll explore:

📌 The different types of bonds and their unique characteristics

📌 How government bonds provide stability and why they’re considered “risk-free”

📌 The role of corporate bonds and the trade-off between yield and risk

📌 Special bond types, including high-yield bonds, inflation-linked bonds, and more

By the end, you’ll have a clear grasp of which bonds suit different investment objectives and how to integrate them effectively into your portfolio.

1. Government Bonds – The Risk-Free Benchmark

Government bonds are issued by national governments to finance spending. They are considered low-risk because they are backed by the government’s ability to tax and print currency to meet obligations.

📌 Key Features of Government Bonds:

✔ Low default risk – Governments rarely default on their debt.

✔ Stable income – Regular coupon payments with low volatility.

✔ Highly liquid – Easily traded in financial markets.

📌 Example: Australian Government Bonds (AGBs)

- Issued by the Australian Commonwealth Government and widely used as a benchmark for risk-free returns.

- Available in fixed-rate, floating-rate, and inflation-linked formats.

💡 Key Takeaway: Government bonds are ideal for investors seeking safety, stability, and predictable income in their portfolios.

2. Corporate Bonds – Higher Yield, Higher Risk

Corporate bonds are issued by companies to raise capital for business operations, expansions, or acquisitions. Compared to Australian Government Bonds (AGBs), corporate bonds generally offer higher yields to compensate for the increased risk of potential default by the issuing company.

📌 Types of Corporate Bonds in Australia:

✔ Investment-Grade Bonds (AAA to BBB-) – Issued by financially stable Australian corporations, these bonds offer lower yields but carry less credit risk. Examples include bonds from major Australian banks (e.g., Commonwealth Bank, NAB) and blue-chip companies.

✔ High-Yield Bonds (BB+ and below, aka “Junk Bonds”) – Issued by companies with higher credit risk, these bonds provide greater returns to attract investors but come with a higher chance of default.

📌 Example: Woolworths vs. Virgin Australia Bonds

✔ Woolworths Bonds (A-rated bond) – A bond issued by Woolworths, a financially stable company with strong cash flow, would be considered investment-grade, offering lower yields but minimal credit risk.

✔ Virgin Australia Bonds (BB-rated bond) – Before its administration in 2020, Virgin Australia issued high-yield bonds to attract investors. These bonds offered higher returns but carried significantly more risk, particularly during periods of financial distress.

💡 Key Takeaway: Corporate bonds can provide higher income compared to government bonds, but investors need to assess credit quality carefully. Investment-grade bonds offer stability, while high-yield bonds carry greater default risk but potential for higher returns.

3. High-Yield Bonds – Should Investors Take the Risk?

High-yield (junk) bonds are issued by companies with lower credit ratings, offering higher potential returns in exchange for increased risk. In Australia, these bonds are often issued by smaller corporations or companies with weaker balance sheets. While they can enhance portfolio income, they come with greater volatility and a higher risk of default.

📌 Pros & Cons of High-Yield Bonds

✔ Higher income – High-yield bonds offer significantly better returns than investment-grade corporate bonds and government bonds.

✔ Potential capital gains – If an issuer's credit rating improves, bond prices may appreciate, creating capital gain opportunities.

❌ Higher default risk – Companies issuing these bonds may struggle to meet debt obligations, especially during economic downturns.

❌ Equity-like volatility – Unlike investment-grade bonds, high-yield bonds can experience sharp price swings, often behaving more like shares.

📌 Example: The 2020 COVID-19 Bond Market Shock in Australia

✔ March 2020 Selloff: Australian high-yield bonds suffered significant losses as investors feared corporate defaults during the pandemic. Sectors such as airlines, energy, and retail were hit particularly hard.

✔ Liquidity Crisis: Many companies with weak financials struggled to refinance debt, leading to concerns about potential bankruptcies.

✔ 2021 Recovery: As the RBA and global central banks provided liquidity and cut interest rates, high-yield bonds rebounded strongly, delivering some of the highest returns in fixed-income markets.

💡 Key Takeaway: High-yield bonds can offer attractive returns for investors willing to accept higher risk, but they require careful selection and risk management. They are best suited for experienced investors who understand the trade-offs between yield and credit risk.

4. Inflation-Linked Bonds – Protecting Purchasing Power

Inflation-linked bonds (ILBs) are designed to protect investors from rising inflation. Unlike traditional fixed-rate bonds, their principal and interest payments adjust based on inflation changes.

📌 How They Work:

✔ Traditional Bonds: Fixed coupon payments, losing value when inflation rises.

✔ Inflation-Linked Bonds: Coupons and principal increase with inflation, preserving purchasing power.

📌 Example: Australian Treasury Indexed Bonds (TIBs)

- Linked to CPI (Consumer Price Index), adjusting payments based on inflation levels.

- Used by long-term investors (e.g., retirees) to maintain real income over time.

💡 Key Takeaway: Inflation-linked bonds act as a hedge against rising prices, ensuring investors don’t lose purchasing power over time.

5. State Government & Semi-Government Bonds – Investing in Australia's Regional Debt Markets

In Australia, semi-government bonds are issued by state and territory governments to finance infrastructure projects such as roads, schools, and hospitals. These bonds play a crucial role in funding public services while offering investors a relatively low-risk fixed-income option.

📌 Why Consider Semi-Government Bonds?

✔ Lower risk than corporate bonds – While not backed by the federal government, they are still considered high-quality debt instruments.

✔ Attractive yields – Typically offer higher returns than Australian Government Bonds (AGBs) due to slightly higher risk.

✔ Diversification – Provide exposure to different regions and economic drivers within Australia.

📌 Example: Australian State Government Bonds

✔ New South Wales Treasury Corporation (TCorp) Bonds – Issued by the NSW government to fund essential infrastructure and services.

✔ Treasury Corporation of Victoria (TCV) Bonds – Used to support Victoria’s public projects, offering yields above AGBs.

✔ Queensland Treasury Corporation (QTC) Bonds – A popular semi-government bond known for its strong credit rating.

💡 Key Takeaway: Semi-government bonds provide an opportunity to earn higher yields than federal government bonds while maintaining strong credit quality. They are ideal for investors seeking stability with a slight premium over sovereign debt.

6. Global & Emerging Market Bonds – Expanding Fixed Income Opportunities

While Australian investors typically focus on domestic bonds, global and emerging market (EM) bonds can offer higher yields and diversification by providing exposure to international economies. These bonds are issued by governments or corporations in developing markets, but they come with increased risks such as political instability, currency fluctuations, and lower credit ratings.

📌 Why Consider Emerging Market Bonds?

✔ Higher yields – EM bonds often offer better returns than Australian or U.S. government bonds.

✔ Growth potential – As developing economies expand, bond values may appreciate.

✔ Diversification – Provides exposure to non-Western markets and different economic cycles.

📌 Example: Investing in Emerging Market Bonds from Australia

✔ Asian Government Bonds (e.g., Indonesia, India) – Higher yields compared to developed nations but subject to political and economic risks.

✔ Latin American Bonds (e.g., Brazil, Mexico) – Attractive returns but carry currency risk for Australian investors.

✔ Global Bond ETFs – ASX-listed ETFs like Vanguard Emerging Market Bond Index Fund (VBND) allow easy access to international fixed-income markets.

💡 Key Takeaway: While emerging market bonds offer compelling yields and diversification benefits, they carry additional risks, including currency volatility and geopolitical uncertainty. Investors should weigh these risks carefully when allocating to global fixed income.

7. Supranational Bonds – Low-Risk Global Fixed Income Exposure

Supranational bonds are issued by international institutions such as the World Bank, the International Monetary Fund (IMF), and the Asian Development Bank (ADB) to fund global projects, infrastructure, and economic development. These bonds are considered highly creditworthy and provide a way for investors to gain international fixed-income exposure with lower risk than corporate or emerging market bonds.

📌 Why Consider Supranational Bonds?

✔ High credit quality – Backed by multiple governments, making them safer than many corporate bonds.

✔ Low default risk – Issuers like the World Bank maintain AAA credit ratings.

✔ Diversification – Provides global exposure while reducing reliance on domestic debt markets.

✔ Ethical Investing – Many supranational bonds fund sustainable development, infrastructure, and environmental initiatives.

📌 Example: Supranational Bonds Available to Australian Investors

✔ World Bank Bonds (IBRD Bonds) – Issued to fund global development projects, carrying very low default risk.

✔ Asian Development Bank (ADB) Bonds – Supports economic growth in the Asia-Pacific region, often appealing to ethical and ESG-focused investors.

✔ Australian Dollar-Denominated Supranational Bonds – Some supranational institutions issue AUD-denominated bonds, making them accessible without currency risk.

💡 Key Takeaway: Supranational bonds offer high credit quality, global diversification, and ethical investment opportunities. They are ideal for conservative investors seeking stability and exposure to international development projects.

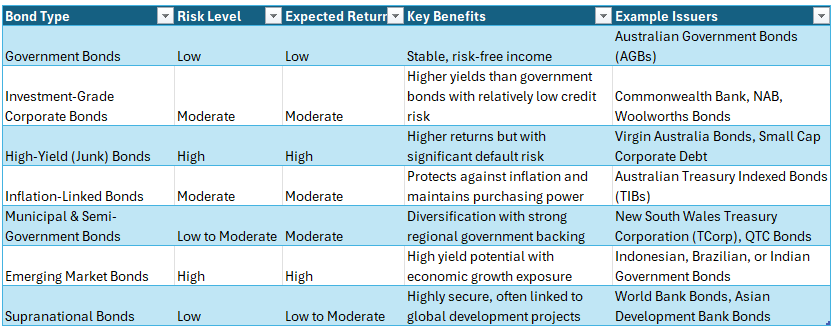

Figure 1: reflects the major bond types summarizing how they compare in terms of risk, return potential, and their role in an investment portfolio.

📌 Final Takeaways: Choosing the Right Bonds for Your Portfolio

✅ Government Bonds – Provide stability and are considered risk-free.

✅ Corporate Bonds – Offer higher yields but come with varying credit risk.

✅ High-Yield Bonds – Potential for big returns but with increased volatility.

✅ Inflation-Linked Bonds – Protect against rising prices and preserve purchasing power.

✅ Municipal & Semi-Government Bonds – Strong credit quality with a regional focus.

✅ Emerging Market Bonds – High risk, high reward, with exposure to developing economies.

✅ Supranational Bonds – Low-risk global exposure, backed by international institutions like the World Bank and Asian Development Bank, often funding sustainable projects.

💡 Key Insight: A well-diversified bond portfolio balances safety, income, and growth potential by incorporating different bond types based on risk tolerance, investment goals, and market conditions.

📌 Choosing the Right Bond Mix for Your Investment Goals

✔ Conservative Investors → Prioritise government bonds and investment-grade corporate bonds for stability and capital preservation.

✔ Income Seekers → Diversify with a mix of corporate bonds, semi-government bonds, and inflation-linked bonds to balance yield and inflation protection.

✔ Aggressive Investors → May allocate a portion to high-yield bonds and emerging market bonds to enhance returns, accepting higher risk in exchange for greater potential gains.

💡 Key Insight: The ideal bond mix depends on your risk tolerance, income needs, and market outlook—striking the right balance ensures long-term portfolio resilience.

📌 Coming Up Next…

Next, we’ll explore "The Australian Bond Market: Who Issues Bonds?", covering:

✔ The key issuers of bonds in Australia

✔ How the government, banks, and corporations raise capital

✔ Where investors can access Australian fixed income markets

🔔 Stay tuned for more fixed-income insights! 🚀📈